From: Ketharaman Swaminathan

To: editet@timesgroup.com

Subject: Cap Two Two UPI Players; Clearly Say, No Free Digi Lunch

This has reference to the opeds entitled Cap Two Two UPI Players by Bikash Narayan Mishra and Clearly Say, No Free Digi Lunch by Ateesh Tankha in today’s Economic Times.

India’s UPI is a world-class innovation. However, beneath the shine lies a serious vulnerability in the form of outsized dominance of just a couple of UPI apps. India must recognise that UPI’s touted zero-fee model isn’t truly free as merchants face hidden MDR and aggregator charges.

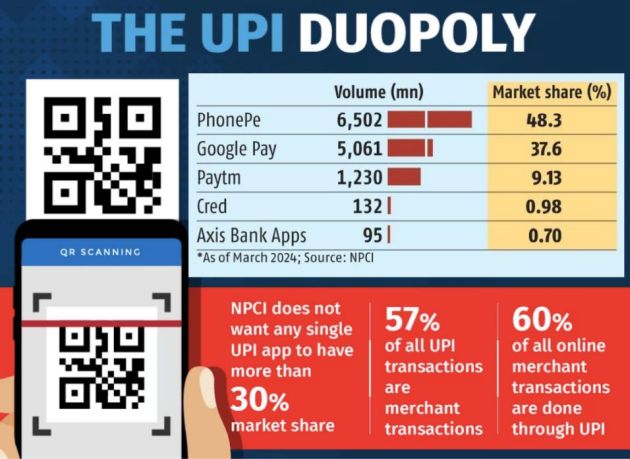

The authors are right about extreme market concentration in the UPI apps business given that over 85% of UPI volumes and value (TPV) are driven by just two American UPI apps aka TPAPs (Third Party App Providers), namely, Walmart PhonePe and Google Pay.

However the remedies proposed by them to eliminate the market concentration are either already in place and ineffective or outrightly impractical.

Let’s have a look at each of them.

Cap Incentives: The authors exhort banks to wean off the top two UPI apps.

This is easier said than done since “a large part of the UPI technology stack is practically managed by top UPI apps like Walmart PhonePe and Google Pay”.

According to Economic Times article titled How Indian banks gave away an opportunity called UPI, and its control, to PhonePe, and Google Pay dated 29 December 2022, banks are busy with their Core Banking Systems (CBS) and, lacking any revenue stream from UPI due to Reg ZeroMDR (see footnote 1), they’re not too keen to spend the resources required to support their UPI infrastructure.

Having effectively handed over their UPI onramps and offramps to the two leading TPAPs, I wonder if banks can ditch them and go to competing TPAPs.

Data Portability: I’ve not come across too many UPI users who are worried about the dominance of PhonePe and Google Pay.

Even if the regulator takes the authors’ advice and stipulates portability of their transaction history and AutoPay mandates, I doubt if consumers will see any compelling reason to switch to other TPAPs. I say this based on what I’ve observed with two other portability initiatives:

- In UK, the banking regulator mandated bank account portability whereby customers are free to move their account from one bank to another, and banks are responsible for migrating their transaction history and direct debit mandates between one another. This didn’t help much. All major banks had devolved to the “least worst” state, each had its own share of disgruntled customers who simply migrated to another bank, the regulation failed to drive any major change in their market shares.

- In India, the telecom regulator mandated mobile number portability. Between my company and me, we’ve mobile phone connections with three Mobile Network Operators. Whenever I’ve visited the office of one MNO, I’ve seen a line of customers of the other two MNOs waiting to port their connections to this MNO. Since I’ve also seen this at the offices of the other two MNOs, it’d appear that each MNO loses some market share and gains some market share. Not surprisingly, there hasn’t been much change in the telecom oligopoly situation.

In my opinion, only analysts and regulators are worried about concentration risk with PhonePe and Google Pay. Unfortunately, they’re not the ones who can move the needle of TPAP players’ market shares. Their customers are and they don’t seem to be bothered too much about which TPAP has how much market share.

I suspect this is why the “Maximum 30% Market Share” rule for UPI apps has still not come into effect even though it was tabled nearly five years ago (see footnote 2).

RuPay-UPI Choice: When UPI was launched in 2016, it supported payments only from savings accounts. During the following 10 years, UPI operator NPCI (National Payments Corporation of India) added a few more funding sources – RuPay credit card is one of them.

I don’t have a RuPay Credit Card. Therefore, I’ve no firsthand experience of making a UPI payment funded by a RuPay credit card. But many others have and complain regularly on X fka Twitter that their UPI-RuPay CC payments failed at many merchants who otherwise accept UPI. This shows that merchants already have a choice of declining RuPay CC-UPI mode, and that they’re increasingly exercising this choice since it attracts MDR.

Small and medium merchants are complaining about inexplicable fees showing up as deductions on E-o-D settlement records for UPI transactions by payment aggregators. Since 2020, UPI has been vociferously touted as a free service to both consumers and merchants. When questioned, payment service providers have claimed that the charges are linked to MDR fees associated with RuPay credit cards, payment instruments that can also be used to make payments via UPI, and which attract an interchange fee (paid by the merchant’s bank to the card-issuing bank in lieu of payment processing, credit risk and fraud protection) of 1.1%, on average, for transactions above ?2,000. When added with other costs like network and aggregator fees, composite MDR for RuPay credit card transactions could easily equal or cross 1.5% of purchase value.

Surcharging: The author claims that merchants are not aware of their right to levy surcharge on RuPay CC-UPI transactions.

I don’t buy this.

Visa and MasterCard repealed their No Surcharge rule on their credit cards over 10 years ago. Many merchants started levying surcharge on their credit cards. But they soon found out that their customers walked out without completing the purchase when they tried to slap a surcharge. Subsequently, most merchants have withdrawn their surcharging practice for credit cards.

Going by this, I’m quite sure that merchants are aware of their right to surcharge a RuPay CC-UPI payment but are taking a conscious decision not to exercise that right because of the fear of losing business from high income customers who prefer credit cards.

RBI MDA: The author observes that “RBI’s ‘Master Direction on Regulation of Payment of Payment Aggregator (PA)’ doesn’t specifically mention the need (for PAs) to educate and receive consent from small and medium merchants about their understanding and willingness to accept intricacies of MDR payments arising from multiple payment instruments”.

At the risk of sounding cynical, I believe this is a feature, not a bug.

The basic business model of banking is to borrow short and lend long. Under the Fractional Reserve Banking system underpinning modern banking, if account holders keep moving their money from one bank to another due to higher interest rates, it might cause severe asset-liability mismatch for some banks, and, ergo, instability of the entire tightly interconnected banking system. So, it’s an open secret among industry insiders that “a bank with sleepy depositors would do well, a bank with antsy depositors would go bust”.

Banking is probably the only industry where the difference between uninformed and informed customers is as big as flourishing versus going bust. Ergo promoting financial literacy goes against the self-interest of banks.

H/T @matt_levine .#SVB #FRB pic.twitter.com/qQb7PHwMCx— GTM360 (@GTM360) March 31, 2023

While on the subject, it might be pertinent to note that, in the entire 70 year history of credit card industry in USA, merchants have perpetually complained about credit card fee schedule being extremely complex but regulators have not done much to clamp down on the obfuscatory pricing practices of credit card networks.

Stalking Horse: The author fears that Payment Aggregators / Payments Solutions Providers might use RuPay CC as a stalking horse in merchants’ transaction volumes to “recoup operating losses associated wtih UPI’s zero MDR protocol”.

I recently observed two vastly different figures for the Total Payments Value share of RuPay CC-UPI:

- 38% according to the second oped.

- 8% according to a recent Economic Times article entitled RuPay is becoming the card of choice; all credit to UPI dated 6 November 2025

Going by such a big discrepancy in the value of the same TPV metric, that too within the same publication, I wonder if the switching between UPI-Bank Account and UPI-RuPay Credit Card modes is already happening.

The reforms proposed in the two opeds to reduce the market concentration in Walmart PhonePe and Google Pay are academically sound but I seriously doubt if they will work in the real world.

In my opinion, the only way to move the needle in the payments business is to target consumers and incent them to switch to BHIM, PayTM, Navi, Cred, and other UPI apps. Of course, incentives like cashbacks will be sustainable only if banks make money from UPI. As long as Reg ZeroMDR is in place, they can’t. As I highlighted in my blog post titled UPI – Too Many Or Not Nearly Enough Players?, not many TPAPs are likely to spend money on customer acquisition since the UPI business currently lacks a revenue model.

Thanks and Regards.

KETHARAMAN SWAMINATHAN

14 November 2025

FOOTNOTE(S):

- Reg ZeroMDR stipulates that banks cannot charge any merchant fees aka Merchant Discount Rate for enabling merchants to accept UPI. This regulation came into effect on 1 January 2020. Initially contemplated for all digital payments including Visa and MasterCard credit cards and debit cards, the final version of the reg covered only UPI and RuPay debit card.

- UPI operator NPCI (National Payments Corporation of India) mandated in 2021 that no TPAP could exceed 30% market share of UPI volumes / values. As India Today reported at the time, “should any UPI service provider found to be in breach of the 30% market share cap, it will have to restrict the onboarding of new users and find ways to dial the number back”.

A condensed version of the above post was not published by Economic Times on 15 November 2025.

In case the aforementioned op-eds titled Cap Two Two UPI Players and Cap Two Two UPI Players in Economic Times are paywalled, cf. following exhibits.