When I sell something to a buyer for 500 rupees and receive a 500 rupee note from the buyer, I don’t pause to analyze fiscal deficits, central bank balance sheets, or the long-term purchasing power of the rupee. I pocket the note and move on – confident that, when I buy something, my seller will do the same.

It’s not like it’s wrong to deep dive into economics. It’s also not like I’m gullible and you can sell me a beachside property in Arizona / London / New Delhi. It’s just that most people don’t get into measuring intrinsic worth of each and every thing – confidence does the heavy lifting in most transactions.

Modern life runs less on verification of intrinsic value and more on a chain of shared assumptions and beliefs. As long as that chain holds, life runs smoothly. Break it, and suddenly everyone starts asking questions they usually ignore.

Consider how often we *don’t* verify things.

Nobody verifies whether the quantity of packaged food they’re buying in a store weighs exactly 500 grams.

When people buy an apartment, the sale deed specifies the square footage. Yet hardly anyone shows up with a measuring tape. They just assume that, when they sell the apartment, the next buyer will also not come with a measuring tape!

When companies factor invoices, banks or NBFCs that provide factoring services rarely validate every single bill with the underlying customer. They run high level checks – names, IDs, patterns – but stop short of full verification. The system works because it usually does. Fun Fact: In some countries, bills are not numbered serially but according to a certain pattern – e.g. Mod10 / Luhn algorithm in Canada – so that the lender can be sure that the underlying artefact is at least a bill in the first place (see footnote 1).

This isn’t irrational. It’s efficient.

Computing intrinsic value in every transaction would be prohibitively expensive. So we outsource trust – to brands, to institutions, to regulations, to market conventions.

Liquidity does the rest. If you know something can be resold at a widely accepted price, you don’t need to independently establish its worth.

Financial markets make this especially clear.

Take stocks. A textbook valuation might say a company is worth $100 per share based on discounted cash flows. But if the stock market price says it’s $200, no amount of intrinsics-based argument will get you the stock at $100. In the moment, ticker is god, price is reality. Intrinsic value may anchor long-term outcomes – but it rarely dictates short-term transactions. C’est la Vie.

That’s so 20th century.

Over 80% of tech IPOs in USA in 2019 were of loss making companies. Still enough people made money on them.

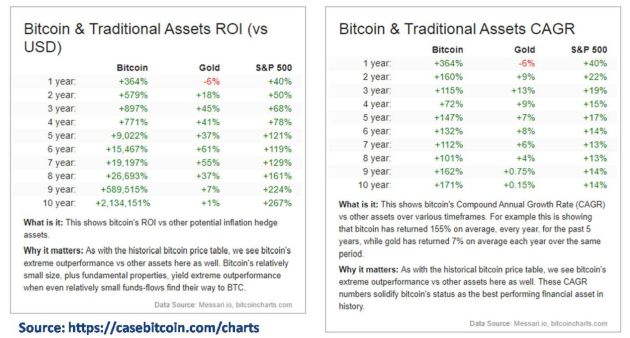

Not many people understand Bitcoin but it’s best performing asset in history.

Extrinsics like hype & liquidity outweigh intrinsics in 21st century.— SKR (@s_ketharaman) November 10, 2021

No longer true since market extrinsics drive stock price way more than company intrinsics. There are so many companies whose PLBS has grown in last two years but their stock price has fallen because of dynamics like ZIRP v. HIRP, geopolitics, etc.

— SKR (@s_ketharaman) November 6, 2023

The same logic extends to currencies, bonds, and newer assets like Bitcoin. Most participants are not continuously computing “true value.” They are relying on the expectation that others will accept the asset at roughly its current price.

Bitcoin is the mother of all examples of “intrinsics don’t matter”: Nobody claims it has any intrinsic worth but it’s the most profitable asset class in history.

This works most of the time.

But most of the time is not all the time.

Sometimes, the chain of trust weakens. Fraud, overleverage, or complacency creeps in. When that happens, systems that ran smoothly on assumptions are forced back toward verification.

- The Enron scandal exposed the fragility of financial statements and SPV (Special Purpose Vehicle) constructs that investors had hitherto taken at face value.

- The 2008 financial crisis revealed how little scrutiny had been applied to underlying mortgage assets.

- The First Brand bankruptcy proceedings revealed that the automobile dealer had double dipped the same set of invoices to multiple parties, which went unnoticed earlier since the factoring service provider did not verify the individual invoices while disbursing the working capital loan.

But these episodes are exceptions and should not invalidate a practice du jour that has been working for a long time.

But they’re not accidents either. They’re the inevitable consequence of a system that optimizes for speed and efficiency over painful and time-consuming validation.

Which brings us to a useful way to think about intrinsics: not as something that always matters or never matters, but as something that matters *conditionally*.

- In highly liquid, standardized markets, intrinsics recede into the background.

- In illiquid, high-stakes, or one-off transactions, they come to the forefront.

- Over short time horizons, price dominates.

- Over long time horizons, intrinsics tend to pull outcomes back toward themselves.

This is why detailed due diligence is the norm in M&A and private equity, but not when buying groceries. It’s why you don’t audit an INR 500 note – but might scrutinize a multi-million dollar investment.

Most of the time, we’re not transacting on intrinsic value. We’re working on the belief that someone else will accept the same terms.

And that belief is usually enough.

Except when it isn’t.

Because in the end, intrinsics are like code beneath a software’s hood: invisible during normal operations but indispensable when the system breaks. You can take the code for granted as long as the software works. But, the moment the software breaks, and the first level blackbox testing does not reveal the root cause, code review is warranted.

Most of modern life works not because everyone measures intrinsic value but nobody needs to when the chain of trust holds. Intrinsics matter when that chain breaks.

FOOTNOTES:

- Ditto taxman when a company submits a bill for claiming tax deduction.