No, there’s no typo in the title.

No, there’s no typo in the title.

In the past, whenever I bought a fridge, washing machine or any other white good item from this leading electronics chain, I’d settle on the brand and model of the product with the store’s sales rep. Before I’d reach the checkout, I’d be accosted by a bunch of sales reps of NBFCs and Fintechs pitching their respective Buy Now Pay Later products at the shopping aisle. I called this “Point of Aisle Finance” in BNPL Ain’t Killing Banks – It’s Making Them Rich in an obvious twist to BNPL’s positioning as “Point of Sale Finance”. At the time, credit card issuing banks did not pitch their BNPL offering at the aisle and totally lost out.

Since then, banks did get rich off of wholesale lending to NBFC and Fintech BNPL providers, as I predicted at the time, but have also jumped headlong into consumer BNPL directly.

When I went to this store last month to buy a new washing machine, I was bracing myself to be ambushed by the sales reps of Bajaj Finservs and ZestMoneys at the aisle. It never happened. Instead, the store sales rep explained the bank’s credit card-based BNPL product. In what’s one of the top five pricing paradoxes I’ve come across in recent times, he offered an INR 1500 discount if I paid in installments instead of plonking cash down.

The sales reps of the NBFC and Fintech BNPLs were lurking behind the checkout counter and didn’t come anywhere near the aisle. It seemed like they were under orders to only convert customers who reached the checkout intending to pay with cash.

Although the bank BNPL offer was tempting, I passed, for reasons that will become clear in a bit. When I told the sales rep that I’d pay with the normal mode on my credit card, he fetched a mobile POS to complete the payment at the shopfloor itself. As a result, I never went to the checkout, and the NBFC and Fintech sales reps didn’t get a chance to pitch their BNPL products to me.

That’s a sea change from my experience just three years ago when I wrote the aforementioned post.

From this datapoint of one, I’m jumping to the conclusion that Bank BNPL is rising and that Nonbank and Fintech BNPL are falling.

There has been a lot of turbulence in the NBFC and fintech industries in the last year or two, both worldwide and in India.

With the end of ZIRP (Zero Interest Rate Phenomenon) in 2022 and the advent of what I call HIRP (High Interest Rate Phenomenon) since then, fintechs have been finding it difficult to raise venture capital.

On top of that, there has been a ton of regulatory scrutiny on many fintech offerings like Banking As A Service (BaaS) in USA; payday lending in UK; recurring payments (Reg Emandate), prepaid credit card (Reg PPI), payments bank (Reg PayTM), business payments solutions providers (Reg BPSP) and unsecured lending (Reg UL) in India (I won’t get into the near-worldwide crackdown on crypto since crypto is not fintech.)

On top of that, there has been a ton of regulatory scrutiny on many fintech offerings like Banking As A Service (BaaS) in USA; payday lending in UK; recurring payments (Reg Emandate), prepaid credit card (Reg PPI), payments bank (Reg PayTM), business payments solutions providers (Reg BPSP) and unsecured lending (Reg UL) in India (I won’t get into the near-worldwide crackdown on crypto since crypto is not fintech.)

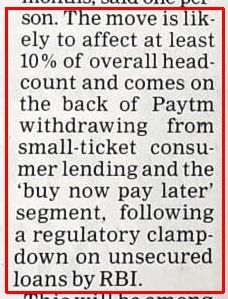

Reg UL is especially relevant for BNPL since it’s a form of unsecured lending. It’s also mostly subprime lending – er, a way to democratize credit, to use the politically correct expression. Concerned over the rapid growth in unsecured loans, India’s banking regulator RBI increased the risk-weights on unsecured credit and bank loans to non-banking financial corporations (NBFCs). The extent of increase is from 100% to 125% for unsecured personal loans and consumer durable loans, and from 125% to 150% for credit cards (Source: Economic Times). Reg UL has severely curtailed the lending capacity of NBFCs and, by extension, of Fintechs (since NBFC is the largest source of capital for Fintech BNPLs).

As a result, the markets have hammered the stock of Bajaj Finance Ltd., the leading NBFC BNPL company of India.

ZestMoney, the leading Fintech BNPL of India, has shut down.

Correlation is not causation but I can’t help thinking that the combination of VC funding winter and regulatory crackdown has crushed the ambitions of nonbank BNPL players.

People below a certain age who are witnessing their first boom-bust cycle in this space often wonder why unsecured lending, which comprises credit card and BNPL, can’t be a “steady business”.

It can’t because people above a certain age remember a time in the early 1990s when a certain public sector bank went berserk and issued credit cards left right and center, racked up huge delinquent outstandings, faced RBI crackdown, and stopped issuing new credit cards for two years until it got its default rate below the regulatory ceiling. Then there was the consumer loan boom in the early 2000s. When it went bust, Citigroup sold its consumer lending business in India. The next boom-bust cycle in the early 2010s saw the exit of the consumer lending units of Barclays and Fullerton from the Indian market.

Andhra Bank in 1990s. Citi and Barclays in 2000s. Fullerton in 2010s. ZestMoney joins a long line of lenders who learned the hard way that it's easy to lend but hard to recover money in a market where loan recovery laws are very pro borrower. https://t.co/AUC20DzeJT

— Ketharaman Swaminathan (@s_ketharaman) February 13, 2024

Going by my experience over the past three decades, unsecured lending will always go thru’ boom-bust cycles, especially in a market like India where per capita income is low and less than 5% of the population is eligible for unsecured loans. Unless the underlying structural issues of demographics are addressed, unsecured lending will continue to have a bumpy ride.

Now, for why I didn’t opt for the BNPL offered on my credit card (or by the NBFC or Fintech).

In the case of Bank BNPL, I needed to swipe – okay, dip or tap – my credit card to get a pre-auth for half the purchase value, and get billed the full purchase value via three EMIs in my next three credit card statements. After paying off the three EMIs, I’d need to approach my credit card issuer bank and ask them to release the pre-auth. All three of my credit card issuers have CSRs with room temperature IQ. I didn’t fancy the idea of jumping through the hoops with them to extinguish the lien, so I decided to pass on the BNPL option despite the 1500 buck discount. (Now, if these banks replace their human CSRs with ChatGPT, I might change my mind!)

7 years after I first asked if a chatbot can replace a human CSR, I have a definitive answer: Yes, chatbots have replaced 700 human FTEs at Klarna.https://t.co/razkPYTU5A https://t.co/QugV3Ht8KO

— Ketharaman Swaminathan (@s_ketharaman) February 28, 2024

In the case of NBFC or Fintech BNPL, all I had to do was dip their card at the POS terminal for only the value of the first installment (aka downpayment), and pay the remaining two EMIs in the following two months. While that was straightforward and frictionless, I’m wary of dealing with fintech BNPLs after going through a shady experience with one of them a couple of years ago. In the course of executing a customer engagement for an eBill vendor, I reviewed the BNPL terms and conditions of Amazon, its fintech BNPL partner and sponsor bank. Although I’d never actually signed up for BNPL, my credit score got dinged. I’m guessing there was a dark pattern somewhere that must have extracted my consent without my knowledge. Therefore, I didn’t bother to find out what the NBFC and Fintech BNPL sales reps had to offer at the checkout counter. I simply paid with credit card and moved on.

On a side note, this is yet another area where the UX / CX of bank sucks compared to fintechs. But banks are probably only paying the price for eschewing dark patterns and sticking to the letter and spirit of the law. Therefore, I’ll file this under Why Banks Will Never Catch Up With Fintechs On UX.