As we saw in Feature Or Bug – Facebook & Tideplus, #FeatureOrBug refers to a feature that masquerades as a bug.

To recap:

As brands increasingly adopt personalization in their communications, what you see is not what I see.

Then there are other types of differences like:

- What you see on desktop is not what you see on mobile

- What you see yesterday is not what you see today

- Inconsistencies in what you see wherever and whenever.

At first blush, it might seem that the discrepancy is caused by a bug in brand websites, apps or messages. But, if we dig deep, we might get the nagging feeling that the brand has deliberately caused the difference i.e. the discrepancy is actually a feature.

In that post and in the follow-on one entitled Feature Or Bug – Housing, LinkedIn, Starbucks, Et Al, I covered many favorable and neutral examples of #FeatureOrBug from Facebook, LinkedIn, Starbucks, and a few more brands.

In this post, I’ll discuss an unfavorable case of #FeatureOrBug.

Frequent users of PayTM will be aware that there are three ways of making a payment with India’s leading e-wallet:

- Method 1: Pay with credit card and other funding sources on file. This method requires two-factor authentication according to the Indian regulator’s mandate. But, by letting you store a card on file, PayTM obviates the need to enter credit card details for each and every transaction. Therefore, the 2FA involved in this step entails less friction and lower risk of failed payments compared to the way most other brands dumbly implement 2FA “as per RBI mandate”

- Method 2: Pay with wallet balance. To use this method, you need to top up your PayTM wallet with funds from your credit / debit card, bank account (or other PayTM users). This step does not require 2FA – or even 1FA.

Did you know that PayTM lets you make a payment w/o entering a single password/PIN? Shows convenience trumps security. Even in India.

— Ketharaman Swaminathan (@s_ketharaman) January 6, 2017

- Method 3: In case you initiate a payment via Method 2 without having enough balance in your wallet to cover your bill, PayTM automatically invokes Method 1, lets you cover the shortfall in-flight from your funding sources on file, and complete your payment in a single pass.

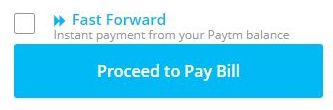

PayTM lets users choose their desired method of payment through the Fast Forward option located above the Proceed to Pay Bill button. If users want to proceed via Method 1, they can leave the Fast Forward option unchecked. If they want to use Method 2, they can check Fast Forward. (Method 3 is system-invoked).

Since I don’t like to block my money in “yet another e-wallet”, I always opt for Method 1 when I pay my utility, phone and other bills with PayTM. Ergo, I never check the Fast Forward option.

Since I don’t like to block my money in “yet another e-wallet”, I always opt for Method 1 when I pay my utility, phone and other bills with PayTM. Ergo, I never check the Fast Forward option.

(#ProTip: If you pay your utility bill directly on your utility company’s website with your credit card, you might be slapped with a Surcharge. Instead, if you use PayTM to pay the same bill with the same credit card, PayTM will eat the credit card processing cost. Not only will it not levy any surcharge, PayTM might even give you a cashback. The double benefit is a form of what’s commonly called “VC Subsidy”. In addition, you might find PayTM’s UX better.)

There’s one exception to my overwhelming preference for Method 1: Uber. When #CurrencySwitch caused a huge cash crunch a little over a year ago, I’d to go cashless for my taxi rides. At the time, the only cashless payment method supported by Uber was PayTM wallet balance and I’d to live with it. Since then, I’ve been keeping some balance in my PayTM wallet to pay for my Uber rides via Method 2.

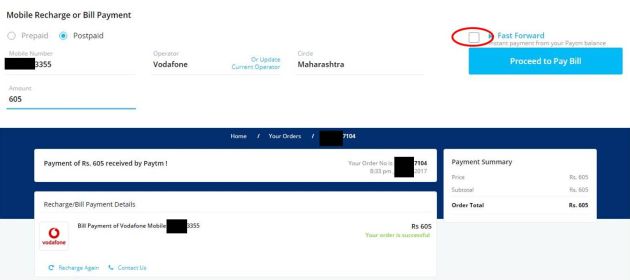

I recently headed over to PayTM to pay a mobile phone bill. As usual, I opted for Method 1 and left the Fast Forward option unchecked. I clicked the Proceed to Pay Bill button and kept my credit card CVV and VbV password handy. However, this time, the website didn’t ask me to enter these two pieces of information. Instead, it made the payment from my wallet balance i.e. Method 2.

In short, I opted for Method 1 but PayTM overrode my preference and used Method 2.

I asked PayTM Customer Care if this was a Feature or Bug.

PayTM CC claimed that I must have checked the Fast Forward option, that’s why PayTM took money out of my wallet. I countered its claim by producing the following screenshot.

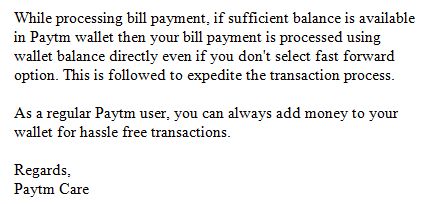

PayTM CC then came back with a different explanation saying that, as long as there’s enough balance in the wallet for a payment, the company had started a new practice of pulling money out from the wallet regardless of whether the customer has checked the Fast Forward option or not. So this was a Feature, not a Bug as it appeared at first blush.

In effect, PayTM told me, “we will take the money from your wallet even if you don’t want us to touch your wallet.”

Now, that’s called pickpocketing in plain English.

PayTM justified its use of Method 2 on the grounds that it expedites the transaction. Since Method 2 does not require 2FA – or even 1FA – it does expedite the payment.

PayTM justified its use of Method 2 on the grounds that it expedites the transaction. Since Method 2 does not require 2FA – or even 1FA – it does expedite the payment.

But it’s still pickpocketing.

I see no difference between PayTM and a supermarket cashier who ignores your request to pay by credit card and pulls out cash from your leather wallet under the pretext of expediting the checkout line.

@vijayshekhar Why does PayTM use my wallet balance when I don't check Fast Forward? Taking my wallet w/o permission is called pickpocketing.

— Ketharaman Swaminathan (@s_ketharaman) October 27, 2017

And PayTM’s patronizing assurance “you can always add money to your wallet” is like the aforementioned cashier telling you, “You can withdraw money from the ATM outside the store to replenish your leather wallet with cash”.

After this incident, I started wondering, if PayTM fools around with my wallet today, what will it do with my card on file tomorrow.

As noted in my previous post, any #FeatureOrBug must favor the brand since it’s introduced by the brand owner.

I got thinking about how this specific #FeatureOrBug would benefit PayTM.

I could think of the following possibilities:

- PayTM acts as the Merchant of Record in Method 1 and incurs MDR cost, which is reportedly 1.5%. Since it doesn’t slap any surcharge on the payer, PayTM eats this cost. The company avoids this cost by resorting to Method 2

- Monies loaded on PayTM wallets didn’t earn any interest in the past. Now, they do: Wallet balances have been moved to the newly created PayTM Payments Bank and, like other banks, PayTM pays interest on them. In Method 2, PayTM exhausts wallet balances faster and thereby reduces its interest burden

- By skipping a trip to the credit card rails in the case of Method 2, PayTM uses less computing power and bandwidth, and hence incurs lower infrastructure cost.

All three benefits of Method 2 drive down costs for PayTM.

I'll believe fintech can disrupt banking the day it hops off the VC gravy train & still manages to provide better CX than banks.

— Ketharaman Swaminathan (@s_ketharaman) June 11, 2015

Amidst pressures from its investors to reduce its mounting losses, VC-funded PayTM is free to take steps to cut costs.

But not pick pockets.

I think a better approach would be for PayTM to remove the Fast Forward option and make it clear that it supported only one method of payment i.e. Method 2. I can then decide whether to “take it or leave it”.

But, to give me the choice and then flagrantly violate it is a breach of trust.

As a result, I began weaning away from PayTM – I now use it only to encash the aforementioned “VC Subsidy”.

Regular readers of this blog would be familiar with my frequent rants about the friction and poor CX in banking, not to mention the nickel-and-diming resorted to by banks from time to time.

However, not once during the course of my dealing with over a dozen banks in half a dozen countries in over three decades have I doubted the integrity of a single bank (Knock on wood!).

With PayTM, it just took a single transaction for that to happen.

Prompted by this incident, I began weaning off PayTM. I found out that Uber India has changed its method for accepting credit card payments. The innovative new workflow complies with the regulator’s 2FA mandate and eliminates the friction of fiddling around with CVV / VbV / OTP at the end of a taxi ride. Soon after making this discovery, I switched the default payment mode on my Uber app from PayTM to Credit Card.

If there’s a lesson in this for PayTM and other fintechs, it’s the old saying about how trust is hard to gain but easy to lose.