I concluded my blog post entitled ROI For Customer ? ROI For Investor with a promise to write a follow-on post on startup investments that are not made in cash.

This is that follow on post.

Noncash investments have been practice du jour in many industries for decades.

During the dotcom era, it was customary for startups to pay for marketing, advertising and legal services in equity i.e. service providers invested in the startups by way of their services. Startups were cash strapped and didn’t have enough cash to pay for these services. The hypothesis was, these startups were going to become rockstars in the following 2-3 years and their equity would go to the moon, so service providers would get many times more money by accepting shares now at par value and selling them later at higher prices instead of insisting on cash upfront. The service provider presumably booked the revenue on day one, moved it to AR, and, when it sold the equity and realized cash, it used some of the proceeds to square off the AR, and booked the reminder as profits.

In 2017, Microsoft invested $200 million in Flipkart (now part of Walmart). The investment was in the form of datacenter on which Flipkart ran its ecommerce platform – not cash. Microsoft booked revenues progressively as Flipkart went about using its datacenter.

General Electric is known as a leading manufacturer of locomotives, turbines, CAT scanners and other core engineering products but it also has a financial services business that provides financing to customers to buy its core engineering products. Woz a time when the financials business of GE generated more revenues – and way more profits – than its core engineering SBUs put together. So much so that FORTUNE magazine shifted GE from the ENGINEERING category to DIVERSIFIED FINANCIALS in its FORTUNE 500 list. Vendor financing of this nature is also common in large IT outsourcing deals between enterprises and IT vendors like IBM / HPE.

All these transactions had an element of circularity but, as far as I know, none of them was called out for being roundtripping.

Cue to the present day. Circular deals abound in AI and other industries.

Microsoft: Microsoft has invested a total of $13 billion in OpenAI. But this investment is not in the form of liquid cash. Instead, it has issued Azure Credits to OpenAI. When OpenAI runs its AI models on Azure Cloud, it burns those Azure Credits, and Microsoft gets to recognize revenues (see footnote 1).

HSBC: Under the Sale and Lease Back model, a company sells a property (e.g. office building, warehouse, or retail space) it owns to an investor or real estate firm, leases back the property from the new owner under a long-term lease agreement, and continues to use the property while paying monthly or periodic lease payments. My first firsthand exposure to the SLB model was the HSBC headquarters building in Canary Wharf, London. At the time, it sounded contrived and pointless to my untrained eye but subsequently I’ve learned that it’s quite common in the Commercial Real Estate (CRE) industry.

HSBC: Under the Sale and Lease Back model, a company sells a property (e.g. office building, warehouse, or retail space) it owns to an investor or real estate firm, leases back the property from the new owner under a long-term lease agreement, and continues to use the property while paying monthly or periodic lease payments. My first firsthand exposure to the SLB model was the HSBC headquarters building in Canary Wharf, London. At the time, it sounded contrived and pointless to my untrained eye but subsequently I’ve learned that it’s quite common in the Commercial Real Estate (CRE) industry.

Nvidia: “Nvidia agreed to purchase $6.3 billion of cloud computing capacity from CoreWeave, in yet another example of the chip company striking a deal to rent its own chips from a third-party cloud business.”

There are many more such deals (see footnote 2).

In all these cases, incremental revenue is big source of returns for the investor (in addition to capital gains and market cap boosts).

All these deals are circular but they’re not cases of rountripping (not legal advice). They appear so arguably because of loose verbiage.

Take the Nvidia-CoreWeave transaction for example. The statement “rent its own chips” is wrong. Nvidia is purchasing “cloud computing capacity”. It’s not renting its own chips. Cloud computing is the output of chips, CPUs, storage, memory, electricity, cooling systems, networking, and so on. In other words, what Nvidia is buying back is much more than chips.

Let’s take a few examples of similar deals from outside tech:

- A farmer sells oranges to Sunkist Growers and buys Sunkist orange juice.

- A limestone quarry owner sells limestone to a cement company and buys cement from the cement company.

- The cafeteria contractor of Block fka Square buys a Square dongle from Block to accept credit card payments from the company’s employees for their meals.

All of these deals are circular but none of them is rountripping (not legal advice).

Roundtripping happens only when the same item is being sold and bought back. Not when there’s a transformation of the former to the latter aka value addition. In none of the above cases is the same item being sold and bought back. In all of the above cases, the item being bought back is value added over the item being sold.

As @Kwebbelkop points out, many things in the modern economy work like that.

In all of the above examples, the noncash investment model has generated incremental revenues for the investing companies. Quite often, it has also boosted the market cap of some or all of the parties involved in the deal.

Sold my couch on FB Marketplace and the guy asked if I want cash or equity in his company.

I love San Francisco.

— Tara Viswanathan (@TaraViswanathan) November 8, 2025

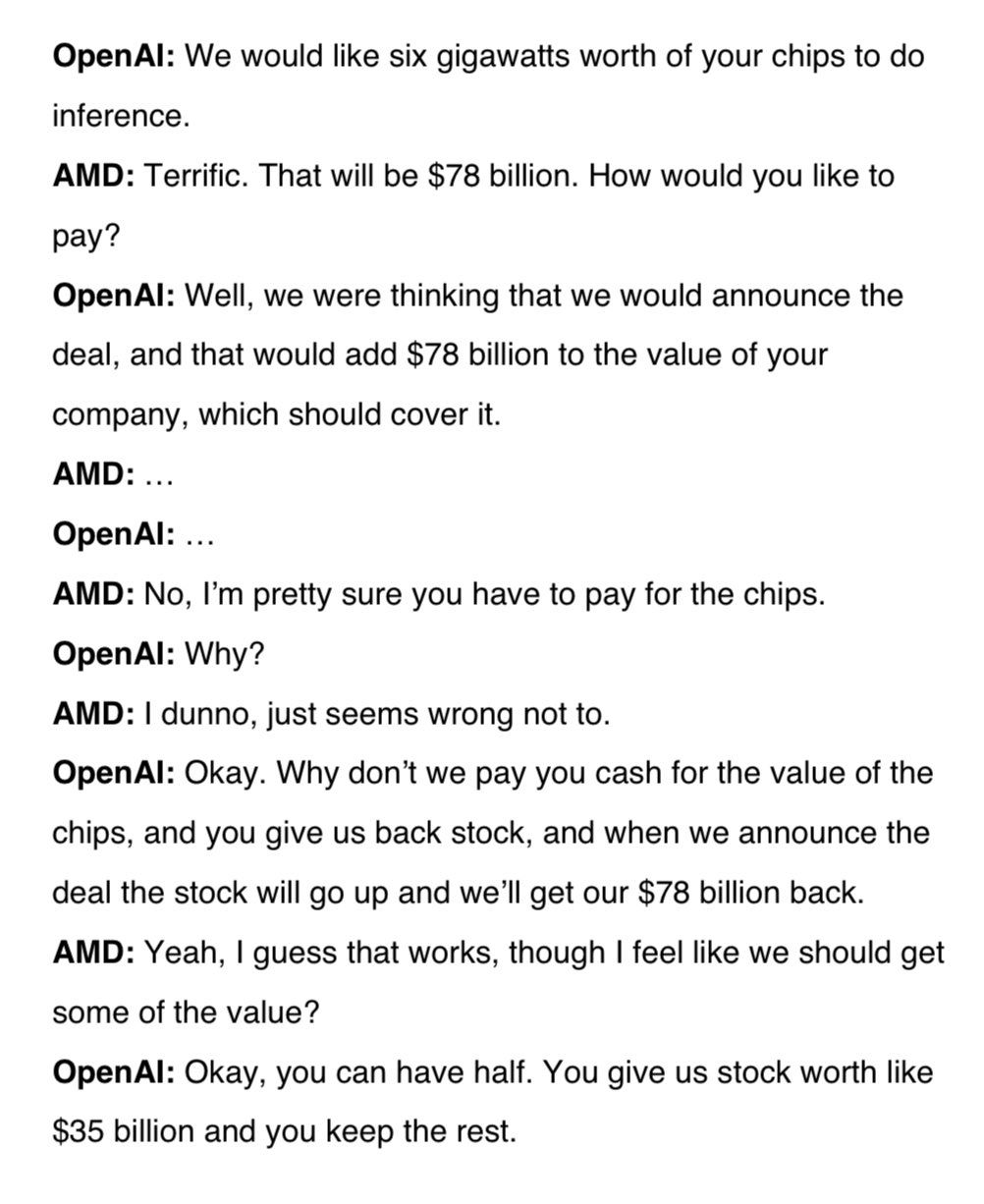

I leave you with this hilarious take on the circular deal between OpenAI and AMD by Matt Levine.

FOOTNOTE(S):

- According to Microsoft’s latest earnings reports, the company has not yet started recognizing revenues from OpenAI.

- One more notable example of a circular deal is the one between Open AI and Thrive Holdings. Per Financial Times via Money Stuff dated 1 December 2025, “OpenAI has taken a stake in Thrive Holdings, a company set up by one of its biggest investors, in the latest of a series of circular deals that have enmeshed the $500bn start-up with its customers, suppliers and backers.”