(This post is a slightly edited version of my answer to the above Quora question.)

Question: Is UPI Hampering Credit Card Business?

Short Answer: No. UPI is actually aiding the credit card business.

Long Answer:

At the height of Kool Aid about UPI in 2016-7, a government honcho predicted that UPI would kill credit card and POS terminals by 2020.

I rate this as one of the most harebrained predictions of all times.

POS did not die by 2020. In fact, its count tripled during the period from 2017 to 2020.

At the peak of re/demonetization, a govt honcho predicted that POS machine will be dead in India in 3 years. 2 years later, the count of POS has shot up from 1.5M to 4.25M. This is going to be the most harebrained prediction of all times! https://t.co/aDtFMsXQwr

— GTM360 (@GTM360) November 11, 2019

Whenever a new entrant gains traction, most people think the incumbent will die.

They’re wrong.

This kind of zero-sum thinking misses the point that multiple players can grow simultaneously in fast growing markets like India. Digital payments has only 40% penetration in India, thus providing massive headroom for the growth of both UPI and Credit Card at the same time.

Even in advanced markets where cashless payments has over 90% penetration rate, it’s still possible for competing digital payment methods to grow together if the overall economy is growing reasonably fast e.g. USA (though not Germany, a moribund economy).

As the following data show, credit card business has grown massively in the last five years.

1. Credit Cards in Circulation

Credit card has been around in India for nearly 50 years (I got my first credit card in 1988, my father had one in 1976). In the first 45 years of the credit card industry until 2020, there were 40 million credit cards in India. In the following five years, the industry added 70 million new credit cards to hit a tally of 110 million credit cards in circulation by 2025 (Source). That’s a trebling in the count of credit cards in five years.

Put another way, the size of the credit card industry doubled in five years compared to the previous 45 years. These five years also saw massive growth of UPI volumes and value.

For the uninitiated, the split of credit cards in circulation in India across the various networks is as follows:

- Visa: 55M

- MasterCard: 40M

- RuPay: 15M

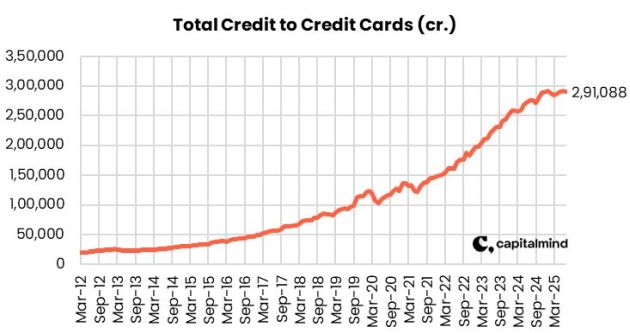

2. Credit Card Outstanding

The TPV (Total Payments Value) of credit cards in India has jumped 3X in the last five years, as you can see from the following exhibit.

On a side note, it’s nost just credit card. There has been an explosion in the volumes of other forms of consumer credit as well in India (see footnote 1).

3. Credit Card Spike Caused By GST 2.0 Shopping

When the reduced GST rate regime came into effect in India on 22 September, there was a massive spurt in shopping between 21 and 22 September. This was reflected in the jump in digital payments TPV between the two days. But all digital payments did not jump equally.

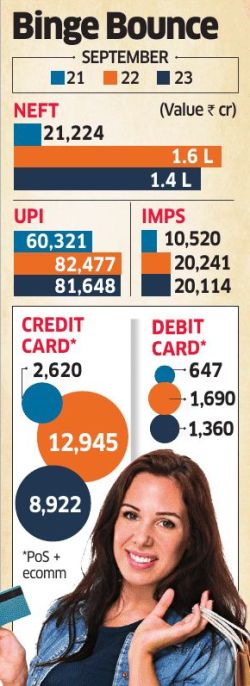

When the reduced GST rate regime came into effect in India on 22 September, there was a massive spurt in shopping between 21 and 22 September. This was reflected in the jump in digital payments TPV between the two days. But all digital payments did not jump equally.

- UPI grew from INR 60,321 crores to INR 82,477 i.e. 37%.

- Credit Card grew from INR 2,620 crores to INR 12,945 crores i.e. 395%.

As you can see, credit card TPV grew more than 10X of UPI TPV. (This is despite the fact that there are 4X fewer credit cards than UPI accounts in India.)

—–

The above data points make it evident that UPI has not hampered the credit card business in India.

In fact, UPI operator NPCI (National Payments Corporation of India) went a step further and acknowledged the explosive growth of credit card in its circular dated 4 October 2022:

“The credit card industry has witnessed significant growth in the country”

Therefore, it can be argued that UPI has boosted the credit card business in India.

—–

This is rather counterintuitive. I advance the following reasons to explain it.

1. Revenues

After Reg ZeroMDR came into effect from 1 January 2020, banks don’t make any money on UPI payments. On the other hand, they earn 2–3% interchange / MDR revenue on credit card. As a result, many banks have gone into an overdrive to issue new credit cards.

In parallel, banks and fintechs like PayTM and Walmart PhonePe have ramped up acquiring by signing up more merchants for credit card acceptance.

2. Greater visibility

When you pay with UPI, you’re spending your own money, so UPI is available as a matter of right. In other words, it’s a democratic product. On the other hand, when you pay with credit card, you’re using your bank’s money. In a low income country, credit card is an elite product. Just as there are many more Maruti 800s than BMWs, there are many more UPI users than credit card users in India.

Before UPI went mainstream, the only way to pay digitally was with credit card. Since there weren’t too many credit cards around, a vast majority of people paid with cash.

After UPI went mainstream, the common man / woman started seeing consumers paying digitally all around them.

i think you’re missing that majority of india paid with cash only.

suddenly paying digitally with additional MDR charges had a negative effect as compared to paying with cards with MDR (which is prevalent in ~ 5% population).

most were new to this. even i was.

— DND (@maybejha) October 28, 2025

This propelled the visibility of the concept of digital payments to a different orbit. People started appreciating that there were other digital payment methods like credit card that came with benefits like rewards, deferred payment, airport lounge access, etc. and applied for credit card at scale.

This may not have happened if UPI hadn’t raised the visibility of digital payments to the next level (see footnote 2).

3. Better fraud protection

I’ve replaced some of my cash and NEFT payments with UPI but I’ve not replaced any of my credit card payments with it. Therefore, UPI has not dented my credit card usage.

That said, some credit cardholders found UPI more frictionless and switched some of their payments to UPI.

But, intimidated by the growing incidents of scam in UPI, some of them have switched back to credit card since it offers better fraud protection. (Besides, contactless / tap-and-go and Visa Direct have reduced friction in credit card payments. Personally, I find it more convenient to use contactless credit card than UPI.)

The retail payments business in India has witnessed classical emerging market dynamics. UPI and Credit Card have both grown sharply in the last five years. (As a matter of fact, even cash in circulation has grown manifold since UPI went mainstream.)

In 2020, when I wrote Don’t Go Global Without Cracking The Value Proposition For Foreign Markets, credit card penetration in India was 3%. In 2025, it’s 8%.

It’s not just data. I can feel the sharp increase in the number of credit cards in circulation around me during these five years!

Even after trebling in size in the last five years, credit card is still underpenetrated, so the credit card business still has a huge headroom for growth in India going forward.

FOOTNOTE(S):

- Economic Times recently reported that Bajaj Finance “took 11 years to get to an AUM of INR 82,400 crores ($9.5 billion). In FY25 alone, it added INR 86,000 crore ($10.1 billion) to its AUM.” For the uninitiated, Bajaj Finance is the largest non bank financial corporation (NBFC) personal loan provider in India.

- A crude analogy would be the impact of Starbucks in India. Before the global coffee retail leader entered the country, a cup of coffee sold for INR 10-75. Starbucks proved that there was a sustained and large enough market for coffee at INR 250 per cup in India. Its market development was followed by a big surge of coffee chains that set shop with prices in the $2.5-$3.5 range. These included domestic chains like Third Wave Coffee and Blue Tokai and international ones like Tim Hortons and Prêt à Manger. Even streetside coffee sellers have doubled or trebled their prices after seeing the acceptance of high priced coffee in the market.