All my life I answered the question in the title of this blog post with a resounding “Of course, I own my shares”.

That changed after I read an article on MIT Technology Review a few years ago.

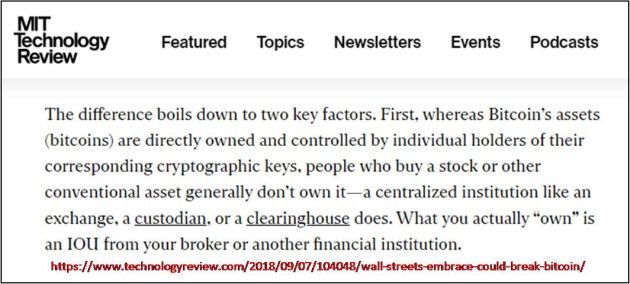

According to @techreview, when you buy shares in dematerialized form, you don’t actually own the shares – a centralized institution like stock exchange, custodian or clearinghouse does. What you own is an IOU from your Broker (or some other Financial Institution).

Since the article didn’t reference any specific country, I tried to find out if it was applicable only to USA or it was true all over the world. Pending clarity, I decided never to open an eTrading / DEMAT account with any nonbank brokerage firm (e.g. Zerodha) since there are greater chances of an unregulated fintech going bust compared to a regulated bank (e.g. ICICIdirect).

“If you buy a stock, you don’t actually own it – a centralized institution like an exchange does. What you “own” is only an IOU from your broker” ~ @techreview .

OMG it means you'll lose your investment if your broker goes bust even if the shares you bought rock.— Ketharaman Swaminathan (@s_ketharaman) October 15, 2018

Faux Patriots / Self Proclaimed Pundits on Twitter asserted that Indian markets are very advanced compared to those in USA / western countries and assured me that shares are held in client’s name with Depositories like NSDL / CSDL.

When clients register themselves on the depository’s website and see their portfolio on its Statement of Holding section, they’re satisfied that the shares are in their name.

But I was not convinced. For three reasons:

- While I can see my shares in my depository account, I cannot withdraw my shares from there.

- My broker trades on my shares held at my depository account. I can’t and don’t. As a result, my brokers enjoys a stronger relationship with the depository compared to me. In the event of a conflict, whose word will the depository take? I thought so too.

- If I spot a discrepancy between my SoH on the depository’s website and my DEMAT portfolio balance on the broker’s website, the exchange tells me to notify my broker, not depository. If all is well with my broker, that’s fine. But if it goes bust, I doubt if my broker will acknowledge and act on my email. (When many TELCOs went bust a few years ago on the back of so-called 2G Scam and AGR, millions of subscribers not only lost their prepaid balances due to the bankruptcy but also forfeited their mobile phone numbers since the failed TELCOs didn’t have any staff to process their porting requests.)

After Karvy fracas, they said, go thru' comms from exchange & report any discrepancies in stock portfolio immediately. But NSE says, take up discrepancies with the broker, which sorta defeats the whole purpose. Wish NSE provides its own email address for reporting discrepancies. pic.twitter.com/BDjSUIUpJq

— GTM360 (@GTM360) December 13, 2019

Meanwhile a leading stockbroker (Karvy) applied for loan with a syndicate of banks and pledged client shares as collateral. The bank accepted the collateral even though shares were supposed to belong to the broker’s clients, and granted the loan. A few years later, the broker defaulted on the loan. The bank encashed the collateral by selling client shares in the stock market.

When I asked the aforementioned Faux Patriots / Self Proclaimed Pundits about this incident, they brushed it off by saying it was a one-off case in which the broker mixed up clients’ shares with its own. (They didn’t seem to realize that it was like brushing off a homicide as a one-off murder.) Nobody could explain why the broker didn’t go to jail for this crime.

Slowly this story dropped out of media coverage by the middle of 2019. (According to media industry scuttlebutt, it costs $X for media to carry your story and $2X for media to not carry your story!)

TIL: Coasian Bargaining: Economics Of Not Doing.

“If you pay me, I will not drill for oil".

"$X to publish your story. $2X to not publish your story".

More lucrative & scalable than economics of doing. https://t.co/sivLEW5jpP .https://t.co/eVMPZe2tuY https://t.co/sivLEW5Rfn— Ketharaman Swaminathan (@s_ketharaman) September 15, 2022

With time, I forgot about it.

Fast forward to last month.

The same story repeated with another broker and bank (BRH Wealth Kreators and HDFC Bank respectively). According to the following article in Economic Times dated 25 May 2022, BRH pledged client shares, took a loan, defaulted on the loan, and HDFC Bank sold the shares to recover its outstandings.

This time the pundits are mum. But I don’t need them to weigh in because the news reports of this incident are comprehensive. By answering many crucial questions that were left unanswered in the Karvy incident, they paint a very grim picture.

SEBI asked the bank how it could sell client shares. The bank fobbed off the capital market regulator saying it had no jurisdiction in banking. SEBI then filed a case against the bank in the tribunal.

The bank produced the depository’s records, which showed that the Broker was the Beneficiary Owner of said shares. Yes, you read that right – according to the depository, your broker owns your shares. Which is exactly what Technology Review had said years ago. Ergo HDFC Bank argued that the regulator’s allegation that it sold client shares lacked merit. It went on to defend its sale of shares by saying that selling collateral to recover outstandings is the SOP of the banking industry whenever a borrower defaults on a loan.

The tribunal has ruled in favor of the bank.

On second thoughts, this shouldn’t come as a surprise – bank accounts have always worked this way.

The money in your bank account belongs to the bank, not you. What you have is an IOU from the bank promising to pay your full account balance on demand.

If the bank goes bankrupt, the IOU is not worth the paper it’s written on. You will get INR 5 lakhs, the maximum amount covered by DICGC insurance. You’ll lose anything above that amount.

Okay, it's now official: Option A, INR 5L.

DICGC was my customer at one time. Otherwise, I'd probably still be under the impression that 100% of deposits in public sector banks are protected by the government. Alas no. https://t.co/VIKN5fqOMI

— Ketharaman Swaminathan (@s_ketharaman) February 1, 2020

Also, it’s not widely appreciated that DICGC insurance excludes current accounts. So, if a bank goes bust, lakhs of crores of money kept by companies in banks vaporizes in an instant.

For the avoidance of any doubt, “bank” in the above context refers to both public sector and private sector banks. In other words, even deposits in public sector banks do not enjoy sovereign guarantee.

On a side note, a major advantage of Central Bank Digital Currency (CBDC) is that your account is held directly with the central bank. Given that the central bank prints notes and mints CBDC, the full balance in your CBDC account enjoys sovereign guarantee, whether it’s kept in a personal savings account or a company current account.

In USA, if a broker goes bankrupt, clients are covered by Securities Investor Protection Corporation.

We work to restore investors’ cash and securities when a brokerage firm fails.

– Video at https://www.sipc.org/ (00:00:20)

I have not heard of “SIPC of India”.

In the case of Karvy, the regulator had ordered the exchange to make clients whole through a special contingency fund. When I last checked, that covered only two-thirds of the loss, with one-third of clients still out of their money / stocks.

Not sure what’s going to happen to clients of BRH Wealth Kreators. The case has gone to Supreme Court. Pending a verdict from the highest court of the land, it’s high time somebody quizzed the regulator on how the market structure allows

- brokers to use client shares as collateral to take a loan for themselves, and

- exchanges to execute orders from banks to sell client shares not owned by them.

The capital markets regulator does have jurisdiction over brokers and exchanges. It’s high time it used that productively instead of going after banks in a lame attempt to lock the proverbial barn door after the horse has bolted.

Bottomline: You don’t own your shares. A financial instiution does. You only have an IOU from your broker.

@s_ketharaman: MIT @techreview is right. Bank says Beneficial Owner of clients’ shares is Broker, not Client. Tribunal rules in favor of bank and against regulator and exchange.