In Don’t Go Global Without Cracking The Value Proposition For Foreign Markets, I’d unpacked the dangers of taking your product global before cracking its value proposition for foreign markets. I’d taken the example of UPI in that post.

Now, I’ll take RuPay, another product from UPI-owner NPCI.

For the uninitiated, RuPay is a homegrown payment card network from India. Launched by National Payments Council of India in 2012, the Indian rival to Visa and MasterCard began life with debit card and subsequently added credit card.

In this post, I’ll explain why I think RuPay has cracked the value proposition for western markets and outline what needs to be done for it to become a runaway success globally.

Value Proposition

Retail payments in Western markets are characterized by the following factors:

Retail payments in Western markets are characterized by the following factors:

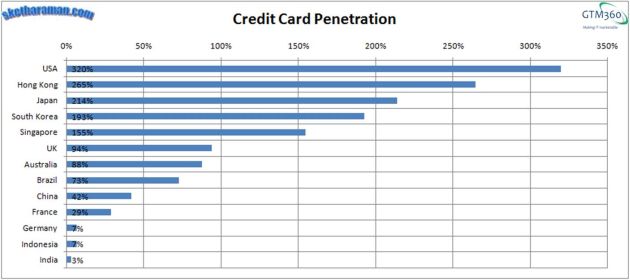

- High penetration of credit card among Consumers e.g. 320% in USA (versus 3% in India)

- High penetration of POS terminals among Merchants e.g. 100% in USA (versus 8% in India)

- Consumers are accustomed to making credit card payments for decades

- All recent payment innovations in the US are on top of card networks e.g. Square, Apple Pay, Apple Card.

Click here for more details.

All of these factors should be music to the ears of any card network. The same factors that will hinder UPI in developed nations will facilitate RuPay.

Therefore, there’s no question that RuPay has strong value proposition for the West.

Alas, that does not mean it will automatically do well there.

To succeed, NPCI needs to

- Wrest control from bureaucrats

- Run RuPay unlike a normal business, and

- Develop GTM strategy.

Wrest Control From Bureaucrats

According to the #ZeroMDR regulation in force since the start of 2020, Merchants incur zero fees for accepting RuPay Debit Card payments. On the other hand, this reg is not applicable to Visa and MasterCard Debit Card and Credit Card payments, so Merchants do incur fees for accepting Visa and MasterCard.

Latest status on scope of #ZeroMDR :

* Applicable for UPI, RuPay Debit Card

* Not applicable for Visa & MasterCard Debit Card & Credit Card

* ??? for RuPay Credit Card.https://t.co/dgJdYkcVqQ . pic.twitter.com/ju0urPJqri— Ketharaman Swaminathan (@s_ketharaman) August 17, 2020

So, Merchants have a strong incentive to promote RuPay against Visa / MasterCard.

Has it helped increase RuPay’s market share?

No, according to MoneyControl article entitled Finance Ministry move on merchant discount rates killing RuPay cards: Study:

IIT Bombay study says since there is nil merchant discount rates on the card, banks may not be able to make any money on RuPay card transactions. As a result, Visa and Mastercard are gaining. The study, Merchant transactions through debit cards – costs and prices, conducted by Professor Ashish Das of the Mathematics department, has found less RuPay debit cards being issued by banks from September 2019 to August 2020. Only 65 lakh debit cards have been issued in the period, compared to 4.6 crore cards in the corresponding period of the previous year, the study found. More Jan Dhan accounts, less RuPay cards. Das argues that this happened when 3.6 crore new Jan Dhan accounts were opened this year, compared to 4.2 crore in the previous year.

Will #ZeroMDR help boost RuPay’s offtake in future? I don’t think so.

To understand why, it’s necessary to understand how card networks operate.

While a full treatment of the subject is beyond the scope of this post, suffice to say that Merchants who wish to accept RuPay need a RuPay Merchant Account. It’s one of the quirks of the card network business that, while NPCI owns RuPay, it cannot issue RuPay Merchant Accounts. Only banks can.

Now, coming back to the MDR fees I mentioned above? That’s a fee levied by Acquirer Banks on Merchants. #ZeroMDR on RuPay means Acquirer Banks don’t make money off of RuPay. Ergo, they have no incentive to promote RuPay. OTOH, #ZeroMDR is not applicable for Visa and MasterCard, so Acquirer Banks do make money by issuing Merchant Accounts for Visa and MasterCard. Therefore, they have a strong incentive to promote RuPay’s competing card networks.

So, even though Merchants would love to accept RuPay and NPCI would love to propagate RuPay, RuPay won’t be a hit automatically.

What appeared in bureaucratic circles to be a great way to promote RuPay seems to have backfired at the end.

The way it looks right now, NPCI needs to wrest control of RuPay from bureaucrats to revive it even in India, let alone take it global.

Card Network Is Unlike Normal Business

In a normal business, there’s a single buyer and a single seller.

Card network is not like a normal business. It’s one of the oldest examples of the so-called “4-corner marketplace” where there are many players who perform complementary tasks but have conflicting interests. What works in other industries does not work in card networks. See payment card value chain for more details.

Created over 50 years ago, Card Networks enjoy the so-called “Network Effect”. While a full treatment of this extremely powerful principle in marketing is beyond the scope of this post, suffice to say that Network Effect drives the huge popularity and extreme longevity of incumbent card networks and makes it difficult for newcomers to displace the incumbents.

In a simple business with one Seller & one Buyer, free can create a hit. But, in a complex 4-corner credit card network, free can lead to a flop.

Or why #ZeroMDR on Rupay has actually given a boost to its competitors Visa & MasterCard.https://t.co/r89dfw3lLA

— Ketharaman Swaminathan (@s_ketharaman) October 5, 2020

Develop GTM Strategy

But difficult does not mean impossible. Somebody has done it. More on that in a bit.

But difficult does not mean impossible. Somebody has done it. More on that in a bit.

Visa and MasterCard are the incumbents in the card network business virtually everywhere in the world including India. RuPay is the new kid on the block.

Zero MDR won’t be enough for RuPay disrupt Visa and MasterCard. (In fact, as the aforementioned MoneyControl article argues, ZeroMDR may disrupt RuPay instead of Visa and MasterCard.)

What will?

As I’d highlighted in my post entitled How To Contain Card Interchange Charges in 2016, for RuPay to make a difference, it needs to offer both debit and credit cards and operate internationally. In other words, NPCI must become a full-service card network with a global footprint.

Let’s see what has happened in the intervening four years:

- RuPay now offers both debit card and credit card. Check full service.

- NPCI recently founded a subsidiary called NPCI International Payments Limited (NIPL), which has the remit of taking RuPay international. Check go global.

Astute readers might guess that this was the strategy followed by China Union Pay. The Chinese card network offers both debit and credit cards. While CUP started locally within China, it quickly took the battle to Visa / MasterCard’s backyard by aggressively expanding to North America and Europe. It’s the only local card network anywhere in the world to have made a dent on Visa / MasterCard.

Emulating China might sound politically incorrect amidst the current border tensions. But, when 95% of POS terminals in India are still imported from China and hundreds of millions of bills are paid in India with Chinese payment apps every month, how verboten can it be for an Indian payments company to copy Chinese strategy in the national interest, huh?

Well 3 years are over. There are 5M POS terminals in India now. 95% of them are from China. Installed base is expected to grow by 10-15% – in this pandemic-struck year. Even a Black Swan couldn't kill POS. https://t.co/p0LQfxaitb .

— GTM360 (@GTM360) August 25, 2020

With good progress being made on those two key elements of GTM strategy, let’s now come to MDR.

Banking is heavily regulated in India. On top of that, 70% of the industry is owned by the government. As a result, #ZeroMDR could be easily enforced in India. But that will be impossible in western markets, where banks are private sector companies and government can’t coerce them to sell a product for free.

That said, debit card interchange has been regulated in the USA and EU for nearly a decade. So it won’t be too hard for NPCI to push through a halving of MDR from its peak rate of 2% for debit card and 3% for credit card with acquirer banks. This will give a compelling reason for merchants to accept RuPay.

Of course, for this strategy to work, RuPay will need to incent issuer banks to match or better Visa and MasterCard rewards on RuPay debit and credit cards. This will require burning a lot of cash, which NPCI must be prepared to do in order to give consumers a compelling reason to apply for and use RuPay cards.

A new card network with 2X Rewards & 0.5X MDR of Visa / MasterCard will be highly disruptive. It won't be profitable. But that hasn't stopped VCs from funding disruptive startups. Will we see such a startup soon? https://t.co/AUMVK1o5Ii #RuPay

— GTM360 (@GTM360) February 7, 2019

NPCI’s international marketing capabilities are a bit crusty now, as illustrated from its confusion regarding country, continent, and region.

"Several countries such as Asia, Africa and the Middle East have displayed interest in UPI …" ~ @NPCI_NPCI via https://t.co/qst47iWkn0

Second Law of International Marketing: Distinguish between Country & Region. pic.twitter.com/88KmoyYEko

— Ketharaman Swaminathan (@s_ketharaman) August 31, 2020

But that’s something that can be improved over time.

RuPay has a strong value proposition for all major markets in the world.

NPCI seems to be on track to execute on the strategy required to promote RuPay in the west and the rest of the world.

Therefore I’m very hopeful that RuPay will become a runaway hit globally sooner rather than later.

Disclosure: A portion of this blog post appeared in my Quora Answer https://qr.ae/pNCK63 .