Consumer advocates ranted about overdraft protection fees in 2008, saying the service was forced down upon consumers.

While the uninitiated can Google “overdraft protection” for a prosaic definition of the term, Stanley Bing offers the following tongue-in-cheek description for one of the most lucrative services offered by US banks:

While the uninitiated can Google “overdraft protection” for a prosaic definition of the term, Stanley Bing offers the following tongue-in-cheek description for one of the most lucrative services offered by US banks:

“No matter what you spend with your debit card, even if you have no money in your account, the guys at the bank will make sure that you’re not embarrassed. They’ll pay your tab!”

In return for having your back, banks charge an overdraft protection fee. Ranging from $20 to $30, this fee is a major source of revenues for American banks.

To appease consumers, the US government passed Reg. E in 2009. The new rule required banks to seek customers’ explicit opt-in for overdraft protection.

Banks went after their customers aggressively to do this. I’d called out marketing campaigns for enrolling consumers for overdraft protection (ODP) as a big opportunity for Indian BPO industry at the time. More on this in my post entitled Overdraft Opt-In Presents A Huge Opportunity For BPOs.

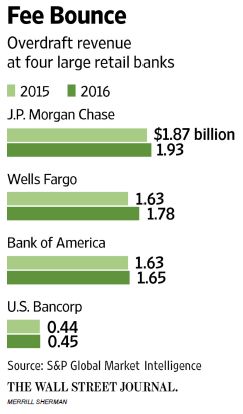

Seven years later, US Banking industry’s overdraft protection business has bounced back to 2009 levels. According to Wall Street Journal, “overdraft fees totaled $33.3 billion in 2016”.

Seven years later, US Banking industry’s overdraft protection business has bounced back to 2009 levels. According to Wall Street Journal, “overdraft fees totaled $33.3 billion in 2016”.

Consumer advocates are now back with a fresh raft of complaints.

In a new lawsuit filed recently, the consumer protection regulator CFPB has charged TCF National Bank with “tricking consumers” into overdraft services by using misleading language that enrolled “people who said yes to a question over the phone about wanting their debit card to continue to work as it had been.”

The CFPB further claimed the bank asked new customers about opting in “immediately after a series of mandatory items the consumer had to agree to in order [to] open the account…most consumers fell into the rhythm of initialing the terms of the agreement and signed on.”

A survey by overdraft regulation proponent Pew Charitable Trusts found that 52% of consumers who have paid a debit-card overdraft fee don’t recall opting in to this service.

Meanwhile, there’s the usual outrage on Twitter:

Would it be great news for everyone if their payments were dishonored & they'd paid late fees to TELCOs et al?

https://t.co/JkjgNRDC3C— Ketharaman Swaminathan (@s_ketharaman) March 17, 2017

IMO these rants are groundless and deserve to be be dismissed summarily. (Maybe sensing this, the guy I trolled on Twitter has deleted his tweet.)

Because, in the final analysis, it really doesn’t matter how consumers signed up for overdraft protection or whether they remember doing so or not.

The only thing that matters is that consumers are incurring overdraft protection fee today ONLY because their bank account ran out of funds while they were paying their latest telephone bill or whatever. Not because they enrolled for their bank’s overdraft protection service several years ago. (In other words, as long as a customer doesn’t bust their bank balance, they won’t be charged any overdraft protection fees today even if they signed up for the service several years ago.)

If their bank didn’t cover the shortfall, their telephone bill would remain unpaid. Their TELCO would slap a late payment fine or even disconnect their phone.

This is the truth about overdraft protection fees.

But that won’t stop the furor. Thanks to the Great Financial Crisis, the reputation of Wall Street has taken a massive beating on Main Street. Unjustifiedly so, in my opinion, for credit rating agencies are ones really culpable for what happened in 2007. More on that in Credit Rating Agencies & The Financial Meltdown. But I digress.

What we’re seeing now is consumer advocates making bank-bashing hay while the GFC bad bank-rep sun shines and the regulator pandering to their every whim.

Some banks are responding proactively with measures to warn customers of the likely occurrence of overdraft. According to the Wells Fargo spokesperson quoted by WSJ, her bank has already provided low-balance alerts and is in the process of introducing a zero-balance alert that will be sent intraday when a customer’s available balance is zero or negative.

I suspect that won’t suffice.

I expect the regulator to ask banks to provide evidence that consumers who are being charged ODP fees had indeed signed up the service. I’m sure banks captured customers’ opt-in confirmations in their systems and will be able to pull out the required proof from their databases quite easily.

But I suspect it won’t end there.

The regulator may tell banks to take the customer’s approval for every overdraft transaction.

The way ODP works today, the approval is onetime. Once the customer says yes to overdraft protection at the point of opening the account – or at any subsequent stage – the bank automatically covers every incident of overdraft without seeking a transaction-specific approval.

Under the new paradigm, the bank will need to notify customers each time they’re overdrawn, ask them whether they want the specific incident of shortfall to be covered, and go ahead only if the customer says yes.

Considering that retail payment systems are highly automated and handle extremely high volumes, it might seem impossible to seek a transaction-by-transaction approval.

But that’s not true any longer.

Banks can readily deploy technologies like 2-way SMS Alerts to manage individual transactions at scale.

The Indian banking industry offers a good example of the use of 2-way SMS Alerts in retail payments. For the past five years or so, everytime a consumer uses their credit / debit card, they get an SMS notifying them of the transaction.

As of now, this SMS is one-way: If a consumer wishes to report the transaction as fraudulent, they have to phone the bank that issued their card. Phone means wait time, hold music, phone tree and, eventually, a live agent who has no clue about the purpose of the call. This poses tremendous friction, especially when the consumer enters the call in an agitated state of mind, having just suffered a fraudulent transaction on their card. As a result, most cardholders don’t feel confident of being able to report a fraud.

To address their concern, the Indian banking regulator Reserve Bank of India has recently stipulated that customers should be able to report fraud by replying to the SMS message they get from their banks. To support this, banks will soon be upgrading their notifications to 2-way SMS Alerts.

Major kudos to RBI for giving a huge boost for #CashlessIndia. Gaming will happen but banks can control it with latest AI / ML tech. pic.twitter.com/iZpiIk2sRn

— GTM360 (@GTM360) July 8, 2017

To explain how 2-way SMS Alerts would work in the context of overdraft protection service, I’ll continue with the example of the aforementioned consumer whose account didn’t have enough balance to cover their telephone bill.

As soon as the bank covered the shortfall, its systems would automatically send out a text message to the customer saying “Your account was overdrawn just now. To make it whole, we charged you a $XX fee. If you want this transaction to stay, do nothing. If you want to cancel this transaction, reply back with NO. If you cancel, your telephone company may slap a late payment charge on you or even disconnect your service”.

If the customer doesn’t respond, the bank does nothing. Both the original payment to the TELCO and the ODP fee stay. If the customer replies with NO, the bank reverses the payment to the telephone company and credits back the ODP fee to the consumer’s account. The TELCO may slap a late payment charge or even disconnect the customer’s telephone connection.

To implement this technology, the bank obviously needs to know the customer’s mobile phone number. This is not a big caveat in India and other countries where people are not so privacy-conscious and give out their mobile numbers freely and where they’d find it virtually impossible to open a bank account without disclosing their mobile numbers to the bank (See Privacy Does Not Equal Security).

However, it’s a big challenge in the USA, where customers don’t usually share their mobile numbers with their banks. So banks will have to find a way to coax mobile numbers out of their ODP-enrolled customers. Given that privacy is a big thing stateside, this step might prove as difficult as getting the customer to opt-in for overdraft protection in the first place!

Marketing campaigns to collect customers’ mobile numbers might become another hot opportunity for the Indian BPO industry.