I have a list of all people who Reply, Like, Retweet my posts on Twitter. It's called skr-engagers. The list happens to include a few people who I follow e.g.…

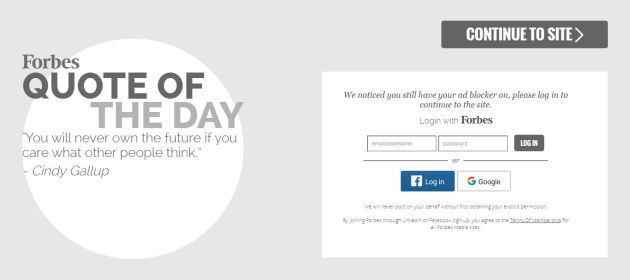

With the rising use of ad-blockers by online readers, the blogosphere is full of advice on how online publishers should move away from advertising and find other ways to monetize…

Many people have reacted vehemently against the government’s move to regulate the creation, distribution and usage of Indian maps under the proposed Geospatial Information Regulation bill. Some have even insinuated…

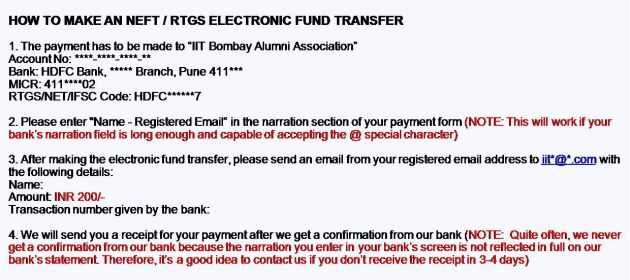

My property management company in UK wanted me to quote the following reference along with my monthly rent payment: MCS MERIDIAN CLIENT ACCOUNT HOUSE RENT 98 MERIDIAN PLACE JUN 2008…

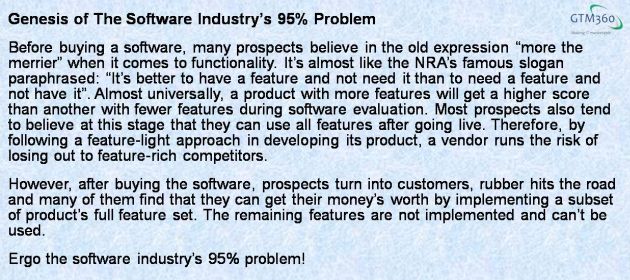

In The IT Industry’s 95% Problem, Gartner Research VP Brian Prentice notes that an average user of a software uses only 5% of the product's features. In other words, 95% of…